June 2026

IPOs, Valuations and Staying the Course

The anticipated public offerings of SpaceX, OpenAI and Anthropic are generating significant investor interest. SpaceX alone is expected to raise more than $75 billion at a valuation approaching $1.75 trillion—potentially the largest capital raise in history. These are genuinely transformative companies, and it is understandable that investors are paying close attention.

Our concern, however, is not with the companies themselves but with the prices at which they are likely to begin trading. At nearly 100 times trailing sales, SpaceX’s expected valuation already reflects years of rapid growth, expanding margins and successful execution. That level of optimism, embedded in the price from day one, leaves little room for error and substantially raises the bar for future outperformance.

This dynamic is not unique to the current cycle. Highly valued IPOs have a consistent pattern of rewarding early insiders, while leaving public market investors with more modest outcomes. By the time ordinary investors can purchase shares, much of the potential upside is often already reflected in the price—and the margin for disappointment is considerable.

The deeper point is that investors do not need to identify the next great IPO to build meaningful wealth. A well-diversified portfolio has historically produced solid, risk-adjusted returns with substantially less volatility. Looking at 20-year rolling periods for the S&P 500, the lowest annualized return was still approximately 6%. That’s without requiring perfect timing, special access or concentrated bets on any single company.

We will continue to monitor the IPO landscape and evaluate whether new public companies represent compelling opportunities relative to their valuations. As always, our focus remains on disciplined, long-term investing—managing risk while preserving and growing your capital over time. We appreciate your continued trust and welcome any questions about how these developments may affect your portfolio.

-The Axiom Team

U.S. and Canadian Markets

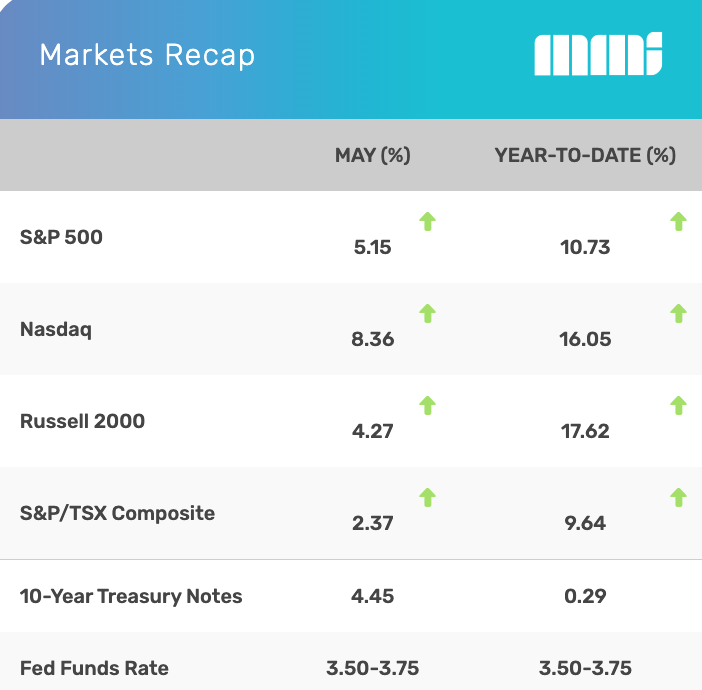

Stocks pushed higher in May, fueled by big tech names, positive economic news, and ongoing diplomatic efforts in the Middle East.

The Nasdaq Composite, which rose 15.29 percent in April, tacked on another 8.36 percent. The Standard & Poor’s 500 Index picked up 5.15 percent, while the Dow Jones Industrial Average advanced 2.78 percent. The S&P/TSX Composite Index gained 2.37 percent.1,2

Choppy Early

Stocks rallied early in the month, notching multiple intraday and closing records amid plenty of volatility. Investors cheered falling oil prices and better-than-expected earnings results from a couple of chipmakers, which lifted the entire tech sector and led the broader averages higher.3,4

Eyes on Jobs

Better-than-expected April job growth fueled a relief rally from investors who were pleasantly surprised that the Middle East conflict had not impacted hiring.5

Despite a hotter-than-expected April inflation report, investors appeared more focused on the U.S.-China diplomatic summit. By mid-month, the S&P 500 had closed over 7,500 for the first time, while the Dow reclaimed the 50,000 level.6,7

A Strong Finish

Kevin Warsh was sworn in as the new Fed chair late in the month, which appeared to bolster investor confidence as all three major averages hit multiple record closes.8

Confidence in ongoing Middle East diplomatic efforts grew, and stocks finished the month on a nine-week winning streak—their longest since 2023—with the Dow Industrials cracking the 51,000 level for the first time.9

U.S. Sectors

Sector performance tells an interesting story about the month.10

Information Technology (+19.76 percent) was the dominant leader and the only sector to post a double-digit gain. Health Care (+2.38 percent) and Consumer Discretionary (+2.13 percent) helped support the rally.10

On the downside, Real Estate (-0.92 percent), Materials (-0.62 percent), and Communication Services (-0.70 percent) were under pressure. Industrials (-0.83 percent) and Consumer Staples (-1.66 percent) also felt some pressure.10

Elsewhere, Financials lost 1.06 percent while Utilities (-5.19 percent) and Energy (-5.63 percent) fell further.10

Canada Recap

Canada’s S&P/TSX Composite Index was under a bit of pressure early in the month as geopolitical tensions and Middle East-driven inflation fears unsettled investors. Oil prices remained high, which weighed on consumer-facing sectors but helped lift energy stocks, one of the largest weightings in the index.11,12

The TSX recovered over the second half of the month, rising steadily as AI chipmakers’ strong Q1 corporate reports lifted sentiment across North American markets, carrying the TSX higher. As the month came to a close, the TSX extended its gains as ongoing diplomatic efforts in the Middle East helped ease some inflation concerns.13,14

What Investors May Be Talking About in June

On June 8th, one of the world’s most influential tech companies kicked off its Worldwide Developers Conference. Hundreds of thousands attend online, while a much smaller group traveled to Cupertino, California, to attend in person.15

Although it’s hosted by one company, the conference has become a seminal event for the industry.15

Expect artificial intelligence to be a big focus again this year. Industry watchers anticipate that some new AI concepts will be introduced, which could cause some ripples in the financial markets.15

World Markets

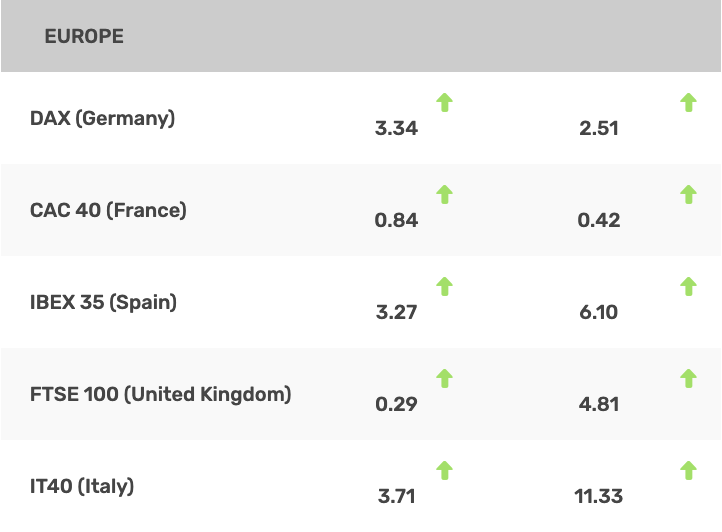

The MSCI EAFE Index climbed 2.60 percent, but the Index underperformed all three major U.S. market averages for the third consecutive month.16,17

In Europe, Spain (+3.27 percent), Italy (+3.71 percent), and Germany (+3.34 percent) notched solid gains. France (+0.84 percent) and the United Kingdom (0.29 percent) lagged a bit.17

Markets outside of Europe were also mixed. Mexico rose 1.08 percent, while India fell 2.78 percent. Brazil (-7.22 percent) was under pressure throughout the month.17

Japan (+11.88 percent) was a top performer in the Pacific Rim. Australia added 0.76 percent, while China’s Hang Seng index lost 2.30 percent. And for the second consecutive month, Korea (+28.45 percent) delivered a 25+ percent gain.17

Yahoo Finance May 31, 2026

Indicators

Gross Domestic Product (GDP)

The economy grew 1.6 percent on an annualized basis in the first quarter, based on the Commerce Department’s second revision of GDP, down from its initial estimate of 2.0 percent. Downward revisions to inventory investment and consumer spending drove most of the overall lower pace.18,19

Employment

Employers added 115,000 jobs in April, versus the 55,000 economists expected. Jobs grew the most in the healthcare, retail, and leisure & hospitality sectors. Unemployment held steady at 4.3 percent last month. Wage growth rose 0.2 percent month over month in April. Year-over-year wage growth increased to 3.6 percent, below expectations.20,21

Retail Sales

Consumer spending rose 0.5 percent in April as expected. Sales at furniture and health & personal-care stores contracted. Interestingly, excluding slower-than-expected sales at gas stations, retail sales rose 0.3 percent month over month. Year-over-year retail sales increased 4.9 percent in April.22,23

Industrial Production

Industrial output rose 0.7 percent in April over the prior month, rebounding from March’s upwardly revised 0.3 percent decline and exceeding expectations for a 0.2 percent increase.24

Housing

Housing starts fell by 2.8 percent in April over the prior month, beating expectations. An unexpected 14-percent rise in multifamily starts offset a 9-percent drop in single-family starts. Regionally, single-family starts rose the most in the Northeast (+16.1 percent) with modest increases in the West (+5 percent) and the Midwest (+2.5 percent), while the South (-11 percent) was the only region where starts fell.25,26

Sales of existing homes rose 0.2 percent in April over the prior month. Increased inflation expectations stemming from higher oil prices pushed mortgage rates higher, putting pressure on sales. Year over year, existing home sales rose 0.5 percent. The median existing home sales price was $417,700, 0.9 percent higher than in April 2025. The supply of unsold homes rose 5.8 percent month over month (1.4 percent year over year) in April to 4.4 months of supply at the current sales rate.27,28

Three months of new home sales data came in last month, previously delayed by government shutdowns. Homebuyers purchased 622,000 newly constructed homes in April, falling short of expectations of 663,000 new home sales. The median new home price rose to $422,500 in April, 8 percent higher than March. The 489,000 unsold new homes in April marked a still-high level of inventory, equal to 9.4 months of supply at the latest sales pace.29,30

Consumer Price Index (CPI)

Consumer prices rose 0.6 percent in April over the prior month, in line with expectations. Higher energy prices (including gasoline) drove over 40 percent of the CPI’s monthly rise. Core inflation, which excludes energy and food prices, rose 2.8 percent year over year, also a little higher than expected.31

Durable Goods Orders

Orders of manufactured goods designed to last three years or longer jumped 7.9 percent in April, the biggest increase in almost a year. Civilian aircraft orders soared 166 percent, with China committing to purchasing 200 planes following a recent U.S.-China presidential summit. Excluding transportation, durable goods orders rose 1.3 percent.32

The Federal Reserve

While there was no Federal Open Market Committee meeting in May, the month was noteworthy for several reasons.

On Friday, May 15, Jerome Powell finished his eight-year tenure as the Chair of the Federal Reserve.

On May 20, the FOMC released minutes from its April meeting, which showed the Middle East conflict has reshaped the Fed’s outlook on interest rates.33

On Friday, May 22, incoming Fed Chair Kevin Warsh was sworn in.34

And on June 16–17, the Federal Reserve will convene its next meeting. That meeting will include a Summary of Economic Projections, including the “dot-plot” of long-term interest rate forecasts.

Copyright 2026 FMG Suite

1. WSJ.com, May 31, 2026

2. TMX.com, May 31, 2026

3. CNBC.com, May 6, 2026

4. CNBC.com, May 7, 2026

5. WSJ.com, May 8, 2026

6. WSJ.com, May 12, 2026

7. CNBC.com, May 14, 2026

8. WSJ.com, May 22, 2026

9. CNBC.com, May 29, 2026

10. SSga.com, May 29, 2026

11. TradingEconomics.com, May 29, 2026

12. TMX.com, May 15, 2026

13. YahooFinance, May 29, 2026

14. TMX.com, May 29, 2026

15. MacRumors.com, May 20, 2026

16. WSJ.com, May 29, 2026

17. MSCI.com, May 29, 2026

18. WSJ.com, May 28, 2026

19. CNBC.com, April 30, 2026

20. WSJ.com, May 5, 2026

21. TradingEconomics.com, May 5, 2026

22. WSJ.com, May 14, 2026

23. TradingEconomics.com, May 14, 2026

24. KPMG.com, May 15, 2026

25. Realtor.com, May 21, 2026

26. Census.gov, May 21, 2026

27. WSJ.com, May 11, 2026

28. TradingEconomics.com, May 11, 2026

29. Realtor.com, May 28, 2026

30. Reuters.com, May 5, 2026

31. WSJ.com, May 12, 2026

32. KPMG, May 28, 2026

33. WSJ.com, May 20, 2026

34. WSJ.com, May 22, 2026

Axiom Financial Strategies Group, LLC (“Axiom”) is a registered investment advisor. Advisory services are offered through Axiom. Securities are offered through Lion Street Financial, LLC (“Lion Street”). Axiom and Lion Street are not affiliated. Advisory services are only offered to clients or prospective clients where Axiom and its representatives are properly licensed or exempt from licensure.

Registration as an investment adviser does not imply a certain level of skill or training. Information about Axiom Financial Strategies Group, LLC can be found by visiting www.adviserinfo.sec.gov and searching by the adviser’s name. This is prepared for informational purposes only. It does not address specific investment objectives. Information in these materials are from sources Axiom Financial Strategies Group, LLC deems reliable, however we do not attest to their accuracy.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

The information herein was obtained from various sources. Axiom does not guarantee the accuracy or completeness of information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. Axiom assumes no obligation to update this information, or to advise on further developments relating to it. Links provided to other websites are not under our control and we are not responsible or liable for the contents of any linked site or any link contained in the linked site. We do not endorse or guarantee and are not responsible or liable for the failure of the products, information, or recommendations provided by linked sites.